We Mapped Every Strata Scheme in NSW. Here's What We Found.

89,452 buildings. Over a million lots. A $562 million market. And 467 companies fighting over it.

Most strata managers can tell you about their own portfolio. A few can name their top competitors. Almost none can tell you the actual size and shape of the market they're operating in.

We can.

UNDA has mapped every strata scheme registered with NSW Fair Trading — 89,452 buildings containing 1,022,775 individual lots. We've linked each one to its current managing agent, geocoded the addresses, estimated contract values, and tracked changes over time.

Here's what the data reveals about the NSW strata management market that nobody else is talking about.

The market is worth up to $562 million annually

Based on our contract value model across all 89,452 schemes, the total addressable market for strata management services in NSW sits between $445 million and $562 million per year. These figures are deliberately conservative — they reflect recurring management fees only and exclude insurance commissions, major works project fees, legal costs, and developer handover fees. The actual market is almost certainly larger.

That's not a number anyone in the industry has published before, because nobody has aggregated the data to calculate it. Individual firms know their own revenue. Industry bodies publish estimates. But the building-by-building calculation — using actual lot counts, scheme types, and graduated per-lot rates — hasn't been done until now.

The market is more concentrated than anyone realises

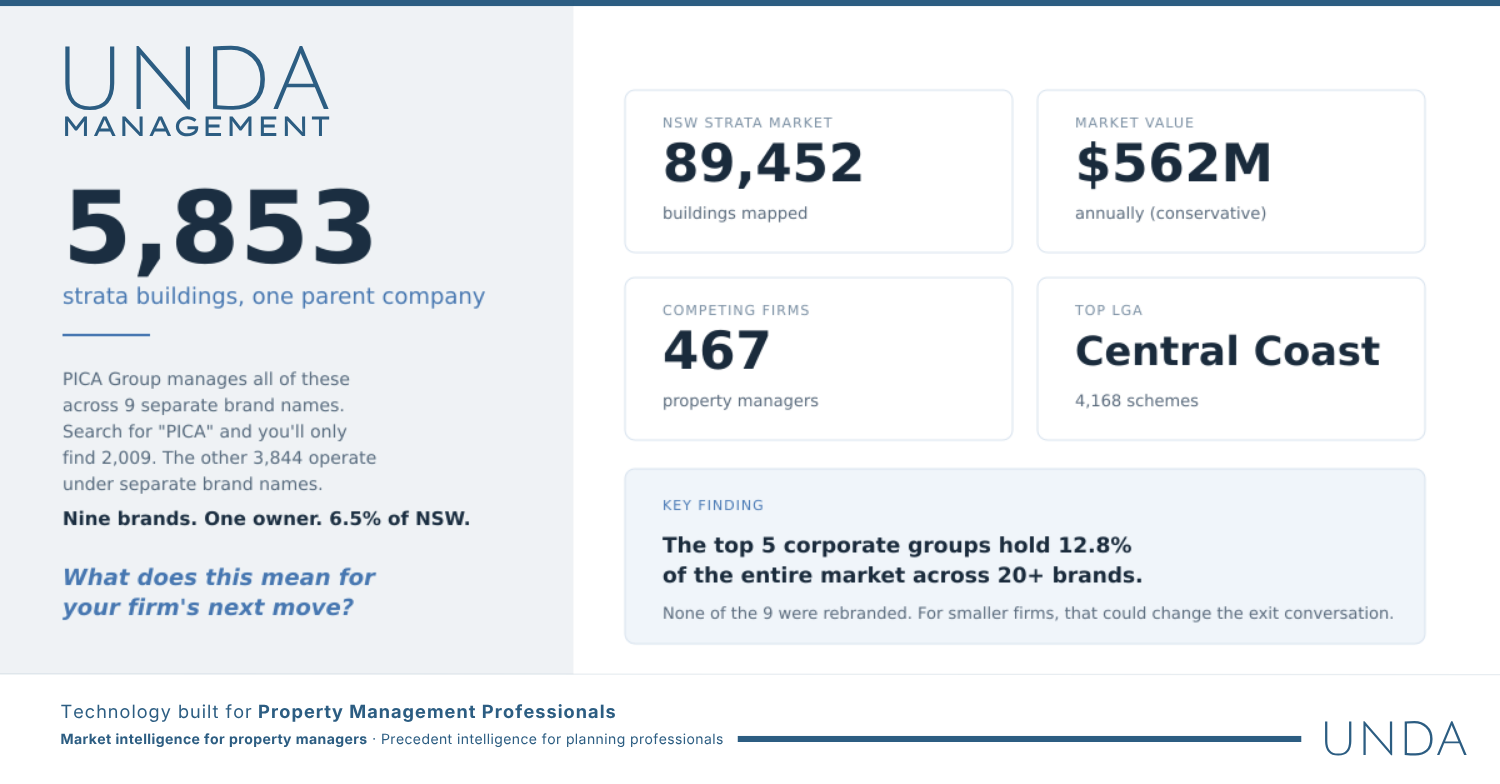

Look at a raw list of NSW strata managers and you'll see 467 companies competing for business. But that number is misleading — because many of those "competitors" are owned by the same parent group.

PICA Group is the clearest example. Search the NSW Fair Trading register and you'll find PICA Services managing 2,009 schemes. Respectable, but not dominant. What the register doesn't tell you is that BCS Strata Management (1,804 schemes), Dynamic Property Services, ACE Body Corporate, NSW Strata Management, and at least four other brands all roll up to the same parent company.

When you consolidate by corporate group, PICA's real footprint is 5,853 schemes across 9 brands — 6.5% of every strata building in NSW, managed through a portfolio of subsidiaries that most building owners wouldn't recognise as connected.

They're not alone. Jamesons Group operates through 5 regional subsidiaries (Eastern Suburbs, North Shore, Northern Beaches, Inner West, and more), managing 1,545 schemes collectively. Bright & Duggan runs at least three brands totalling over 1,700 schemes.

The top 5 corporate groups control roughly 11,500 buildings between them — nearly 13% of the entire market. When you factor in the long tail of 447 independent operators, many running fewer than 50 schemes each, the competitive landscape looks very different from what the raw numbers suggest.

The question every mid-tier firm should be asking isn't just "who are my competitors?" — it's "who actually owns my competitors?"

The biggest strata markets aren't where you'd expect

Ask anyone in the industry where the most strata activity is, and they'll say Sydney's Eastern Suburbs or the Lower North Shore. The data tells a different story.

Central Coast leads all of NSW with 4,168 strata schemes — more than any single Sydney LGA. Canterbury-Bankstown is second at 3,516, followed by Northern Beaches at 3,477. Sutherland (3,308) and Randwick (2,582) round out the top five.

The City of Sydney — the CBD and surrounds — ranks fourteenth at 1,991 schemes. Fourteenth. The geographic centre of the property industry isn't even in the top ten for strata density.

This matters for business development. If you're allocating sales resources based on assumptions about where the buildings are, you're probably allocating them wrong. The growth corridors are in the suburbs, not the city.

467 managers, one dataset

Perhaps the most striking number is the simplest one: 467. That's the total number of distinct strata management companies currently operating in NSW.

In a market worth over half a billion dollars annually, 467 companies are competing for the same pool of buildings. Some are national operators running thousands of schemes. Others are sole practitioners managing a handful of buildings in their local area.

What separates the firms that grow from the ones that stagnate? In our experience building this dataset, it comes down to information asymmetry. The managers who know where the opportunities are — which buildings are coming up for renewal, which competitors are overstretched, which suburbs are underserved — are the ones winning new business.

The rest are waiting for tenders to land in their inbox.

What this means

The NSW strata management market is large, fragmented, and poorly understood — even by the people operating in it. Most managers are making strategic decisions about growth, pricing, and territory based on incomplete information.

UNDA Management exists to change that. We've built the dataset that shows the full picture: every building, every manager, every suburb, every contract cycle. If you're a strata management professional who wants to compete on intelligence rather than guesswork, that's what we do.

This is the first in a series of data-driven analyses of the NSW property market. See our companion analysis: We Analysed 853 Waverley Panel Decisions. Here's What Gets Approved →

About UNDA Management

UNDA Management provides market intelligence for strata managers — 89,000+ NSW schemes mapped, every manager linked, every contract cycle tracked. Our sister product, UNDA Development, provides precedent intelligence for planning consultants. Learn more at unda.management